North America and APAC report solid economic growth while EMEA wanes.

By Larry Basinait

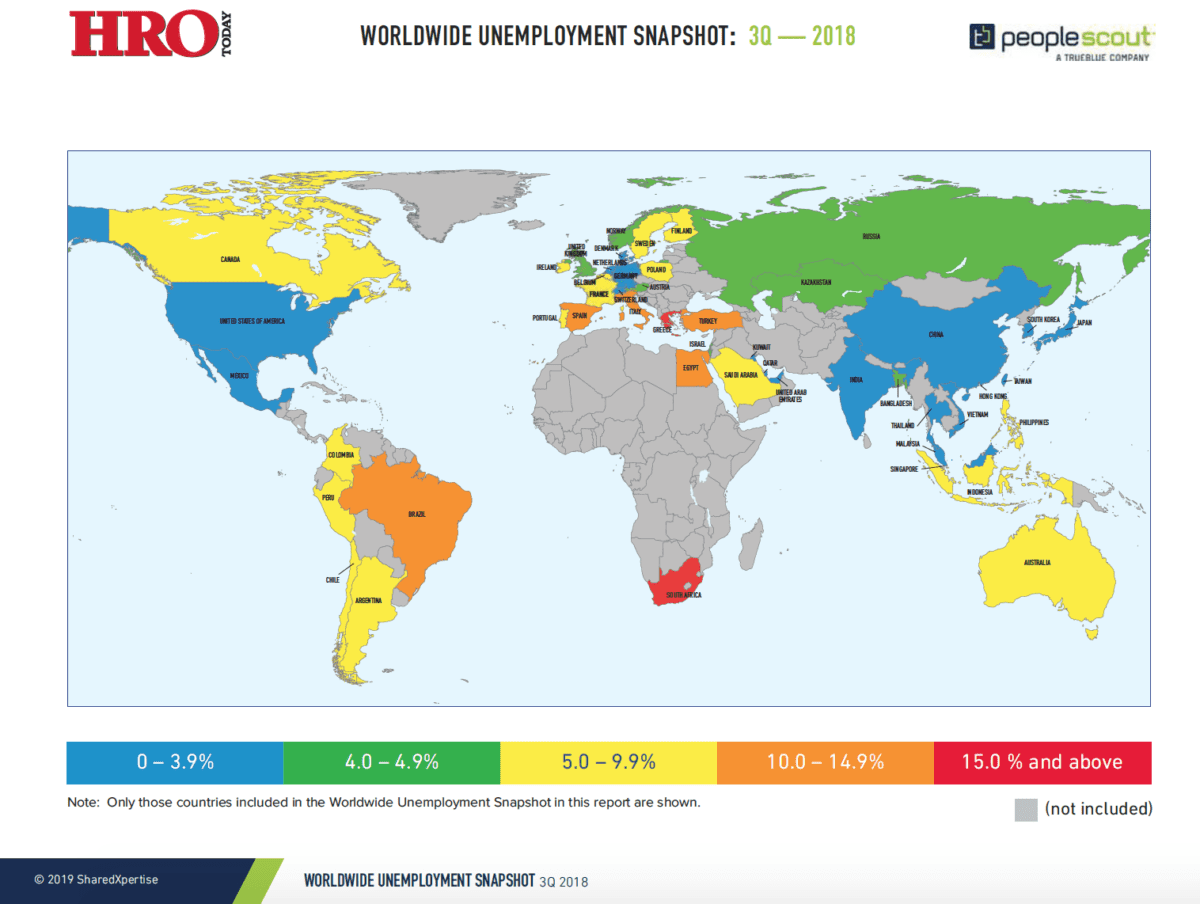

Deploying a global workforce and ensuring access to the best talent is a crucial component of success for all multinational enterprises. Global labor market intelligence is an invaluable tool for HR departments and can be used to inform critical decisions around the best countries and regions in which to grow. PeopleScout, a global provider of RPO, MSP, and total workforce solutions, has partnered with HRO Today magazine to produce quarterly reports that compile current international labor market figures, including measures such as national Gross Domestic Product (GDP), unemployment rates, and population estimates.

To truly understand unemployment rates, it is necessary to collect several categories of market information about the overall economic environment from which they derive. For that reason, this report also analyzes measures that include GDP, economic forecasts, and other factors that offer insight into a given country’s economic circumstances.

As the June 2018 Global Economic Prospects Report documents, the global economy seems to be leaving the legacy of the past decade’s financial crisis behind. About half the world’s countries are experiencing an increase in growth. This synchronized recovery may lead to even faster expansion in the near term as strong growth in large economies like China or the United States spills over to other parts of the world.

Many forecasts for 2019 reflect optimism. Additionally, economic growth is occurring for the right reasons; investment and trade increases have risen once more. Furthermore, in the United States, Japan, and parts of Europe, unemployment declined while inflation remained steady, suggesting that policymakers may have found that “sweet spot” in the tradeoff between unemployment and inflation. Global growth is projected to end up at 3.1 percent for 2018, but may edge down over the next two years as global slack dissipates, trade and investment moderate, and financing conditions tighten, according to World Bank.

North America

According to the Bureau of Economic Analysis, real GDP in the U.S. increased by 3.4 percent in the third quarter of 2018, though that was down from the very robust 4.2 percent in the second quarter. Tax cuts for individuals and a budget deal that raised federal spending early in the year helped elevate growth in the third quarter. Consumer spending increased 4.0 percent and federal outlays rose by 3.3 percent.

In September, the U.S. unemployment rate was 3.7 percent, an improvement from the end of the second quarter’s rate of 4.0 percent. Unemployment rates at 5.0 percent or just below are considered by many economists to be at or near full employment. Full employment means that unemployment has fallen to the lowest possible level that will not cause inflation.

The National Bank of Canada reports the Canadian unemployment rate decreased slightly by 0.1 percentage points in September to 5.9 percent, which is almost a record low for the country. Real GDP expanded at an annual pace of 2.0 percent in the third quarter as contributions from trade more than offset a small drag from domestic demand, the latter hampered by weak business investment due to trade uncertainties. Those uncertainties decreased because of the U.S.-Mexico-Canada Agreement (USMCA), which replaced the North American Free Trade Agreement (NAFTA).

Asia-Pacific (APAC)

In the third quarter, higher oil prices sent economic growth in East and South Asia (ESA) to the lowest level in the past year. Nevertheless, the region benefited from tight labor markets and supportive public policies in countries such as China and South Korea. According to an estimate for the region produced by FocusEconomics, ESA countries grew an aggregated 6.1 percent year-over-year in the third quarter, down from the 6.4 percent expansion in the second quarter. Overall, economists see the ESA region expanding by 6.0 percent in the fourth quarter.

China has by far the largest economy in the region with a GDP of more than $14 trillion and is nearly three times larger than the second biggest economy, Japan, which has a GDP of $5.2 trillion. In the third quarter of 2018, unemployment in these top two regional players once again decreased from already low rates, with China reporting 3.8 percent unemployment and Japan at a remarkable 2.3 percent. But despite the low unemployment rate, economic growth slowed in China in the third quarter.

India has the third largest economy in the region with a GDP of $2.8 trillion and the second largest population at nearly 1.3 billion. Its unemployment rate remains an enviable 3.5 percent. Early estimates are that economic growth in India likely softened in the third quarter due to a worsening trade deficit and concerns about the health of the banking sector.

Europe, the Middle East, and Africa (EMEA)

The largest economies in EMEA, with the notable exception of Germany, posted improved unemployment statistics. Yet in spite of the positive employment data, the Eurozone economy slowed notably in the third quarter. GDP grew a seasonally-adjusted 0.2 percent -the worst result in more than five years. The sharp deceleration is expected to be partly due to one-off market shocks, especially as car production in the quarter was disrupted by new emissions standards. That said, the Eurozone economy has clearly entered a slower growth trajectory after an excellent performance in 2017, according to FocusEconomics.

Germany has the eighth largest population in EMEA at 83 million and by far the largest GDP ($4.2 trillion) in this region. But even with this in mind, its economy contracted for the first time in more than three years, a driving force behind the weak third quarter reading overall.

In contrast, France’s economy picked up pace in the third quarter. France is the region’s third largest economy but had a fairly high unemployment rate of 9.3 percent in September. A recovery in household spending was behind the improved result, and an end to strikes led to higher expenditures on energy and transport.

Brexit uncertainties grew more severe during the third quarter, with a decline of workers from the Eurozone in the U.K., exacerbating its tight labor market. The economic slowdown in the Eurozone is expected to be temporary and economists project the region to expand by 0.4 percent in the final quarter of the year, finds FocusEconomics.

Latin America

Early estimates revealed that growth in the Latin American economy was unchanged in the third quarter, as uneven dynamics across economies kept activity moderate. Regional GDP growth (excluding Venezuela) came in at 1.6 percent in third quarter -one of the worst results seen in the past year and a half. However, overall, 2019 is poised to be a better year for the Latin American economy. Regional growth (excluding Venezuela) is expected to improve to 2.3 percent from the 1.7 percent projected for 2018, finds FocusEconomics.

Looking at the South American economies with available GDP data, growth waned in Chile and Peru in the third quarter. Chile’s economy expanded at the slowest pace in a year while Peru’s economy also grew at its slowest rate since the first quarter of 2017. The unemployment rate dipped very slightly compared to the second quarter of 2018 for two of the larger economies in the region, Chile and Peru.