A sector-by-sector review of the HR services market.

By Gary Bragar

NelsonHall‘s global business process services (BPS) market forecast reveals that the overall HR services market will grow by 5.8 percent in 2018. Growth is being driven across all HR service and technology markets as more organizations look to leverage HR partnerships and HR platforms with the goal of enabling digital transformation and a high-performance operating model. NelsonHall research analyzes the performance of the HR sector in 2018 and offers predictions of what is to come in 2019.

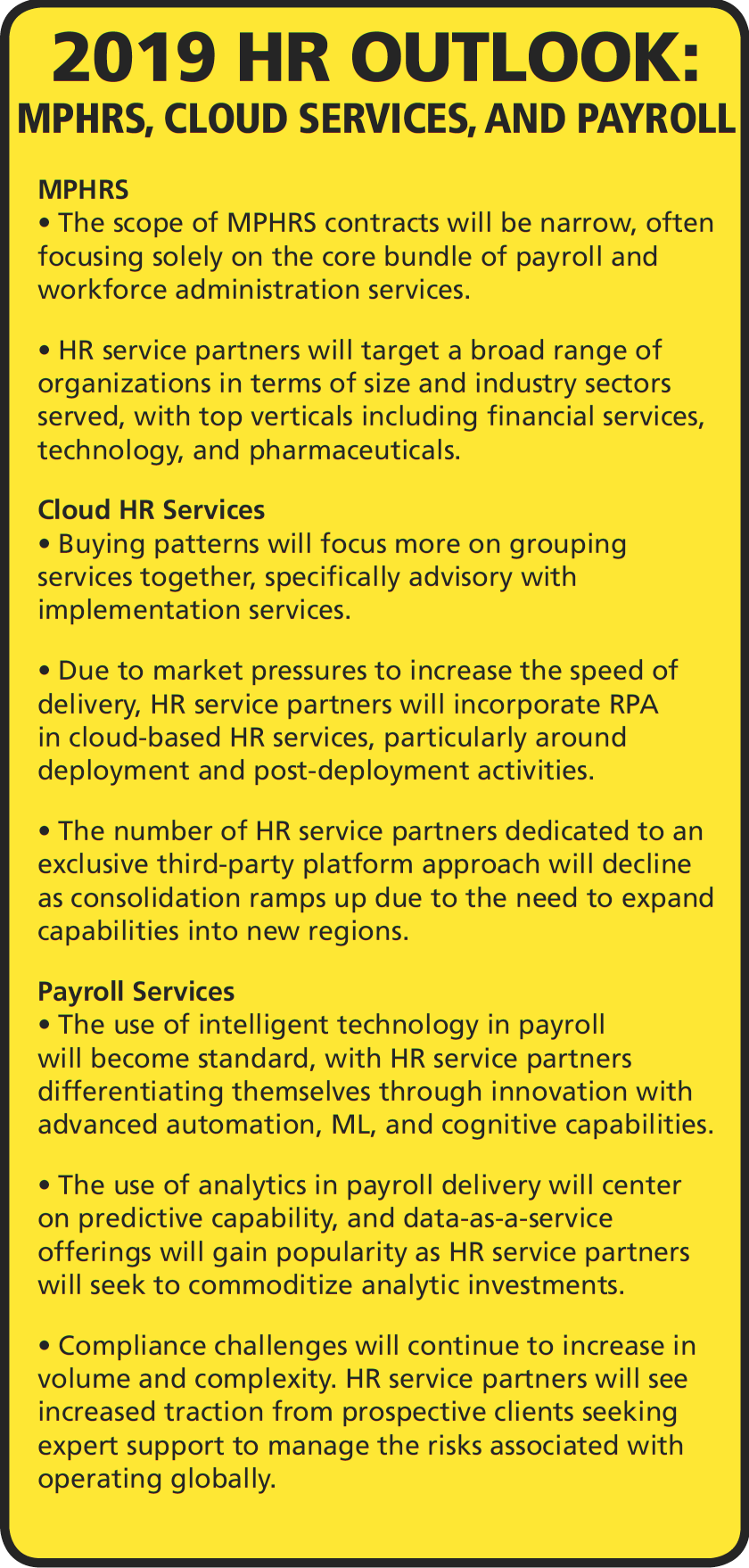

1. Multi-process HR services (MPHRS) stay relevant. While MPHRS contracts and revenues are in decline and steadily being replaced by cloud-based HR services contracts, they are still important to HR leaders seeking the benefits of having one partner, one contract, and one governance structure for the provision of multiple HR services. MPHRS contracts still make sense when HR service partners have specialized capabilities and proven results for each of the HR services in scope. On average, current MPHRS contracts include three HR service lines.

Currently about 40 percent of multi-process HR deals are being delivered on a cloud platform, leaving a significant opportunity for HR service partners to support HR leaders seeking a shift to the cloud. By the end of 2019, NelsonHall expects the cloud to reach an inflection point and surpass on-premise deals as the majority. Also coming up: acquisition and partnership activity centered on the expansion of global capability into APAC and Oceana, and strengthening of robotic process automation (RPA), machine learning (ML), and data analytics capabilities.

2. Payroll services remain a mainstay. The payroll market is healthy, with HR leaders focused on technology-based managed services. More often, HR service partners are seeing organizations looking to solve global payroll within 12 months after a move to the cloud. HR and payroll need to work closer than ever on payroll transformation initiatives and technology alignment strategies.

2. Payroll services remain a mainstay. The payroll market is healthy, with HR leaders focused on technology-based managed services. More often, HR service partners are seeing organizations looking to solve global payroll within 12 months after a move to the cloud. HR and payroll need to work closer than ever on payroll transformation initiatives and technology alignment strategies.

The mid-size market (between 500 and 15,000 employees) remains the largest segment of the payroll market with 47 percent market share. It’s also the fastest growing at a 6.2 percent compound annual average growth rate (CAAGR), primarily due to the demand for increased control of payroll operations and implementation of cloud software solutions. The sweet spot in terms of client size for several HR service partners is around 5,000 employees, as evidenced by payroll services contracts.

Acquisition activity within the market is helping HR service partners strengthen their global capability and cloud-based platforms; add cross-currency and expat payment services; manage the payment of contingent and international workers; and enhance analytics capabilities. HR service partners are expanding their global footprints to include new offices and centers in Africa, and offering new services including deeper analytics offerings and more dynamic integrations to better shuttle data within the HR technology ecosystem.

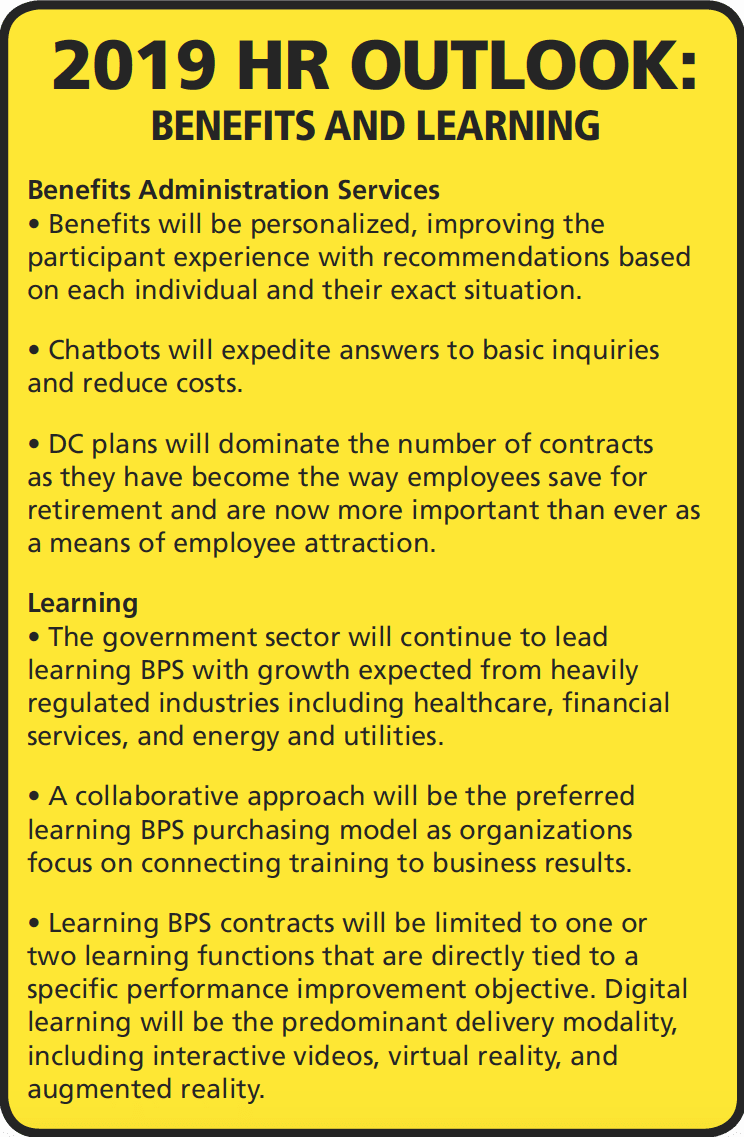

3. Benefits administration services continue to evolve. Defined contribution (DC) benefits contracts are the majority of contracts being announced. Employer DC plans such as 401(k)s are increasingly important as many companies have eliminated their defined benefit (DB) pension plans. DC contracts include the public and private sector, and mostly range between 3,000 and 30,000 participants and between $100 million and $2 billion in assets managed. Health savings accounts (HSA) also continue to rise as a means of saving to pay for the high cost of consumer-driven healthcare plans, while providing a tax break similar to traditional IRAs.

Acquisition activity includes the strengthening of DB and DC plans, EAP, financial wellness, and advocacy services. Partnerships will enable employee feedback; streamline employee benefits management; add RPA, ML, and data analytics; and allow for integration of platforms. New service offerings include employee well-being and healthcare decisions and financial wellness.

Acquisition activity includes the strengthening of DB and DC plans, EAP, financial wellness, and advocacy services. Partnerships will enable employee feedback; streamline employee benefits management; add RPA, ML, and data analytics; and allow for integration of platforms. New service offerings include employee well-being and healthcare decisions and financial wellness.

4. Learning services are being leveraged for employee growth. The majority of organizations are currently seeking learning services to improve standardization and efficiency of the training function. The government sector accounts for the greatest proportion of learning BPS revenues due to high contract values. Manufacturing leads the private sector, followed by high-tech and financial services.

Acquisition activity includes expanding pharmaceuticals and life science capabilities and partnering to strengthen cyber-security training and digital e-learning.

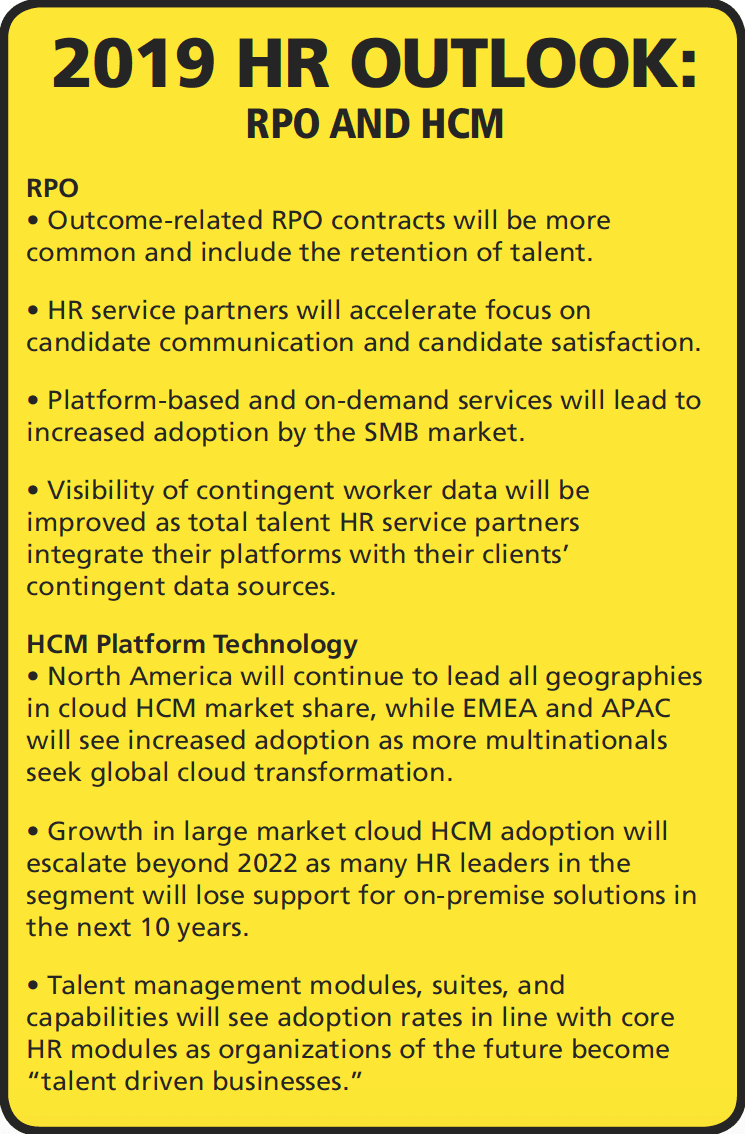

5. Recruitment process outsourcing (RPO) continues to be leveraged by organizations of all sizes. RPO is the fastest growing HR service line, with growth coming from large, mid-size, and small markets. HR leaders are seeking HR service partners’ expertise for candidate attraction, cost savings, scalability, access to tools and technology, and improving quality of hire. Multi-country contracts make up nearly 31 percent of all RPO contracts, spanning two or more countries in a single region (16 percent), multi-regional contracts (7 percent), and global RPO contracts (8 percent).

Acquisitions will strengthen global RPO and talent advisory services, expand IT recruitment capabilities, and enhance AI capability. Partnering with these providers will improve contingent labor recruitment, talent matching, and analytics capabilities.

6. HCM platform technology helps support strategic initiatives. Cloud technology is currently at the heart of digital transformation as businesses of all sizes seek to remain competitive within their industries. Cloud HCM platforms are increasingly in demand as HR leaders seek to leverage technology in line with the business to transform operating models and support strategic initiatives.

HCM technology growth is equally split across all segment sizes, slightly led by the mid-size market seeking HR technology to support growth and compete for top talent. The top HCM modules purchased are commonly core HR and payroll, with demand for talent management modules rapidly increasing.

Acquisitions in the HCM space are commonly focused on adding niche capability and have centered on broader AI and ML as well as predictive and prescriptive analytic capabilities. Partnering in the HCM space remains a key focus area for HCM HR service partners, as more organizations are seeking to leverage best-in-breed solutions to derive custom HR technology ecosystems through APIs and advanced integrations. All major HR service partners expect to double or even triple their partner marketplaces in the coming year to support client demand.

Acquisitions in the HCM space are commonly focused on adding niche capability and have centered on broader AI and ML as well as predictive and prescriptive analytic capabilities. Partnering in the HCM space remains a key focus area for HCM HR service partners, as more organizations are seeking to leverage best-in-breed solutions to derive custom HR technology ecosystems through APIs and advanced integrations. All major HR service partners expect to double or even triple their partner marketplaces in the coming year to support client demand.

Module expansion will center on talent management, with learning, performance, and succession planning all key focus areas of HR service partners’ roadmaps. Further, ML, AI, and NLP tools for “conversational HR” with digital assistants and more deeply embedded prescriptive and predictive analytics are all gaining momentum. HR service partners’ expansion and targeting is focused on continental Europe, Australia, and engaging with on-premise customers seeking a move to the cloud.

Gary Bragar is the HR outsourcing research director for NelsonHall.