A look at the top findings from our 2017 studies.

By The Editors

Industry research is core to human capital management and decision-making. That is why in 2017, the HRO Today research team took a deep dive into several topics that presented challenges to HR professionals: candidate engagement, Millennial preferences, global unemployment, worker confidence, company reputation, and more. Here, we share some of the top findings -the full version of each report can be found on our website.

PASSIVE VERSUS ACTIVE

Today’s top recruitment challenge is no longer identifying and sourcing talent. It’s engagement: Keeping candidates interested and active throughout the recruitment process. A new research report on Candidate Engagement from Hudson RPO and HRO Today uncovers how recruiters and hiring managers are grabbing candidates’ attention and keeping it.

Today’s top recruitment challenge is no longer identifying and sourcing talent. It’s engagement: Keeping candidates interested and active throughout the recruitment process. A new research report on Candidate Engagement from Hudson RPO and HRO Today uncovers how recruiters and hiring managers are grabbing candidates’ attention and keeping it.

The study examines the engagement techniques that hiring managers and recruiters report are the most effective and compares them to what candidates say is most effective. The results highlight where and when hiring managers and recruiters are spending their time and resources most effectively.

The research also makes a clear distinction between active and passive candidates. Active candidates, meaning those that are actively looking or casually looking a few times a week, comprise only 25 percent of the U.S. workforce, or 63 million workers. The lion’s share of the workforce are passive candidates, described as reaching out to their personal networks, open to talking to a recruiter, or completely satisfied/ did not want to move. This group totals nearly 190 million workers in the U.S.

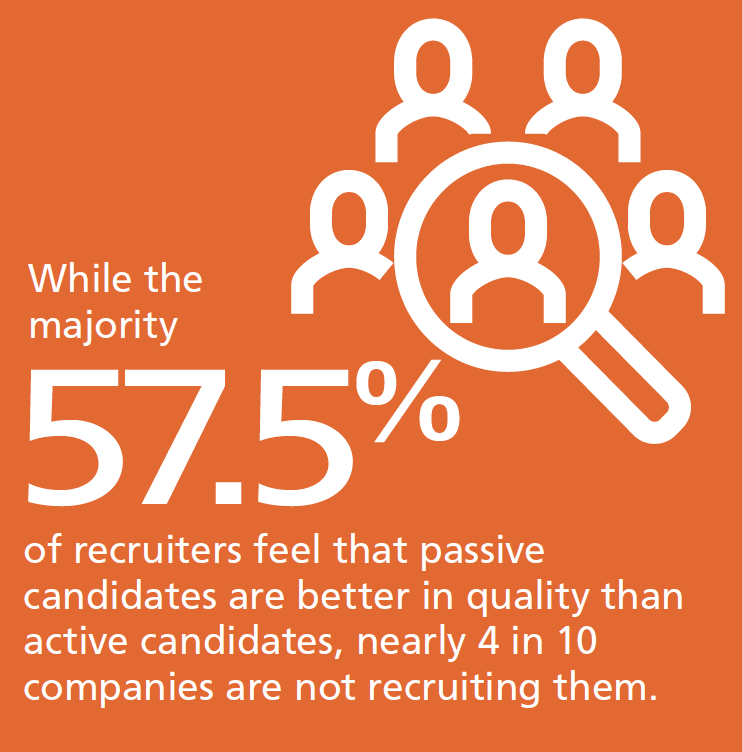

While the majority (57.5 percent) of recruiters felt that passive candidates are better in quality than active candidates, nearly 4 in 10 companies are not recruiting them. Why? Because it’s harder to do. In fact, 82.6 percent of recruiter respondents felt they had to be more aggressive in their recruitment methods, with 40 percent indicating they had to be significantly more aggressive. Recruiters reported they had to contact a passive candidate an average of three times before they could be considered active.

While the majority (57.5 percent) of recruiters felt that passive candidates are better in quality than active candidates, nearly 4 in 10 companies are not recruiting them. Why? Because it’s harder to do. In fact, 82.6 percent of recruiter respondents felt they had to be more aggressive in their recruitment methods, with 40 percent indicating they had to be significantly more aggressive. Recruiters reported they had to contact a passive candidate an average of three times before they could be considered active.

Passive and active candidates research information about job openings and companies through similar sources. A key difference between the two groups, however, is that passive candidates rely far more on their own networking sources -including personal contacts, LinkedIn network contacts, and direct referrals -as opposed to published sources. Recruiting this group means accessing the networks they look to for information, which is more complex than traditional job boards or LinkedIn postings.

When being contacted by recruiters, candidates prefer email messages far above all else, with phone calls and LinkedIn messages coming in second and third. While LinkedIn is ranked as the sixth most effective way to reach passive candidates, it is the most common method used to contact them. LinkedIn is a very useful tool, but recruiters may be too reliant on it.

See more here.

UNDERSTANDING INNOVATION

What innovation concepts are most relevant to the talent acquisition function? A recent study from Alexander Mann Solutions and HRO Today seeks to answer that question -and to understand innovation and the driving forces behind a failure among organizations to innovate.

What innovation concepts are most relevant to the talent acquisition function? A recent study from Alexander Mann Solutions and HRO Today seeks to answer that question -and to understand innovation and the driving forces behind a failure among organizations to innovate.

In the quest to understand innovation, the research study discovered that talent acquisition professionals are facing a challenge that is termed here as “non-novation.” This occurs when HR executes initiatives with the intent to drive new and meaningful change, but somehow the change does not happen. Innovators implement change. Non-novators take a detour.

The research also examined different areas of talent acquisition where innovation comes into play. There was great interest in several types of metrics and workforce planning concepts, including predictive analytics designed to assess a candidate’s potential success; strategic workforce planning; and leveraging unstructured data.

While interest was high around these strategies, they were implemented by fewer than 10 percent of respondents.

Two-thirds (66.7 percent) of respondents report the best way to evaluate new technologies is by seeing them in action -and in person. This means attending in-person user group meetings. In-person user group meetings or conferences allow participants to actively engage with potential solution providers and their existing users.

Candidate engagement techniques associated with candidate experience was a top area for implementing innovation. Simplified applications and automated onboarding were the first and third most frequently cited techniques in terms of interest among respondents.

Looking forward, predictive data and analysis was rated as an innovation area with the greatest potential.

See more here.

RECRUITING DRIVING REVENUE

The impact of hiring the right sales people at the right time cannot be overstated. Without sales driving top-line revenue, every other part of the organization -including operations, marketing, and finance -will fail no matter how well these departments have executed their responsibilities. Recent research from HRO Today and WilsonHCG shows that while 58 percent of recruiters track the cost per hire of a sales position, they don’t have clarity on the cost of not hiring quickly. This means HR managers are often lacking the information they need to make the best recommendations regarding the urgency needed in hiring sales representatives.

The impact of hiring the right sales people at the right time cannot be overstated. Without sales driving top-line revenue, every other part of the organization -including operations, marketing, and finance -will fail no matter how well these departments have executed their responsibilities. Recent research from HRO Today and WilsonHCG shows that while 58 percent of recruiters track the cost per hire of a sales position, they don’t have clarity on the cost of not hiring quickly. This means HR managers are often lacking the information they need to make the best recommendations regarding the urgency needed in hiring sales representatives.

The study also revealed that HR managers don’t have the information they need to best convey to the C-suite the importance of keeping their sales team fully staffed. Organizations can quickly lose thousands -or even millions -of dollars in sales if there are openings left unfilled for longer than necessary. A fully-staffed sales team is critical to the bottom line.

By applying findings from the study into the Sales Force Recruiting Calculator (a free web-based tool on HROToday.com), the impact on revenue of unfilled sales territories is clear. For example, a medium-sized company with 100 sales representatives would see a reduction in revenue of $4.5 million per year when experiencing average turnover, average days to fill, and average revenue per sales territory.

On the other hand, organizations can see a positive impact on revenue when they reduce the average time-to-fill rate. For example, a company with 100 sales representatives that reduces their time to fill by 10 percent (from the average of 58.1 days) would see nearly $500,000 in increased revenue. The same company would see an increase of $1.4 million if there was a 30 percent reduction.

HR’s use of sales force data in recruiting has impacts in other ways, including:

Among the 58 percent of respondents that do track cost per hire, the average is more than $4,000. This amount is exclusive of the opportunity cost of lost sales early in a new hire’s tenure, training, first-year salary, and incentives.

Among the 58 percent of respondents that do track cost per hire, the average is more than $4,000. This amount is exclusive of the opportunity cost of lost sales early in a new hire’s tenure, training, first-year salary, and incentives.- The average time to fill a sales role is 58 days. This means that for every representative that leaves an organization, it takes more than one-quarter of the number of working days in the year to replace them, a huge loss in sales potential.

See more here.

WHAT MATTERS TO MILLENNIALS?

With so much riding on millennials’ contributions, just how different are millennials’ expectations from those of the other generations before them? This isn’t the easiest question to answer.

With so much riding on millennials’ contributions, just how different are millennials’ expectations from those of the other generations before them? This isn’t the easiest question to answer.

What makes millennials truly unique is their lifelong use of technology -they are the hashtag generation. Using mobile technology and continuously accessing social media has given them almost instant access to data and ideas -and the means to share their own. That is not the only real difference, but it’s the key difference, and it profoundly influences how they will team with others and react to all forms of communication. In order to better understand this group and how to best communicate with them, Advantage xPO partnered with HRO Today to examine the preferences and behavioral patterns of millennials with those of Gen X (in this study, between 35 and 49) and baby boomers (in this study, between 50 and 60).

While there are differences between millennials and other generations, they still want what employees from all prior generations have always wanted from an employer: a good benefits package, a positive work environment, and suitable compensation. However, as their presence continues to grow in the workplace, it does not necessarily mean a massive overhaul of workplace culture.

Other key study findings about millennials’ expectations and their implications include:

- The influx of millennials means there’s a more multigenerational workforce than there has been in decades. Millennials’ tech-savvy characteristics contrast with the traits of Generation X, which grew up during the beginning of the computer age, and baby boomers, who have had to adapt mid-career to a technology-based environment. Millennials can help Gen Xers and baby boomers navigate unfamiliar territory. When it comes to the learning business, however, the roles reverse: Millennials are eager to be mentored.

Overall, millennials are a very collaborative group, often looking for a teamwork-based environment over one based on individual accomplishments. Technology facilitates collaboration, and experience and guidance can be shared through technology and traditional means as well.

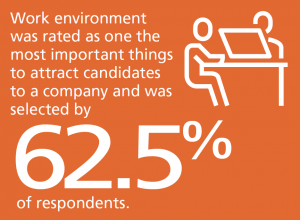

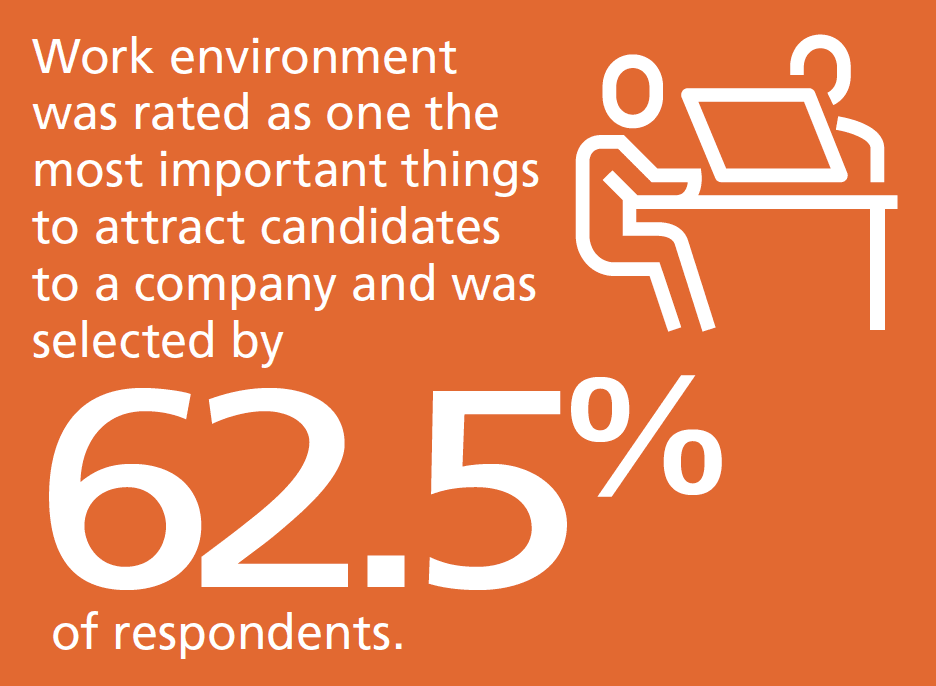

Overall, millennials are a very collaborative group, often looking for a teamwork-based environment over one based on individual accomplishments. Technology facilitates collaboration, and experience and guidance can be shared through technology and traditional means as well.- Work environment was rated as one the most important things to attract candidates to a company and was selected by nearly two-thirds (62.5 percent) of respondents. Digging down deeper into what components of work environment are most crucial, the research confirmed that work-life balance was the key element, particularly for millennials. But for this group, it’s more a work-life “blend” than “balance.” In fact, this study found that workplace flexibility supersedes other factors in importance, surpassing even total compensation.

See more here.

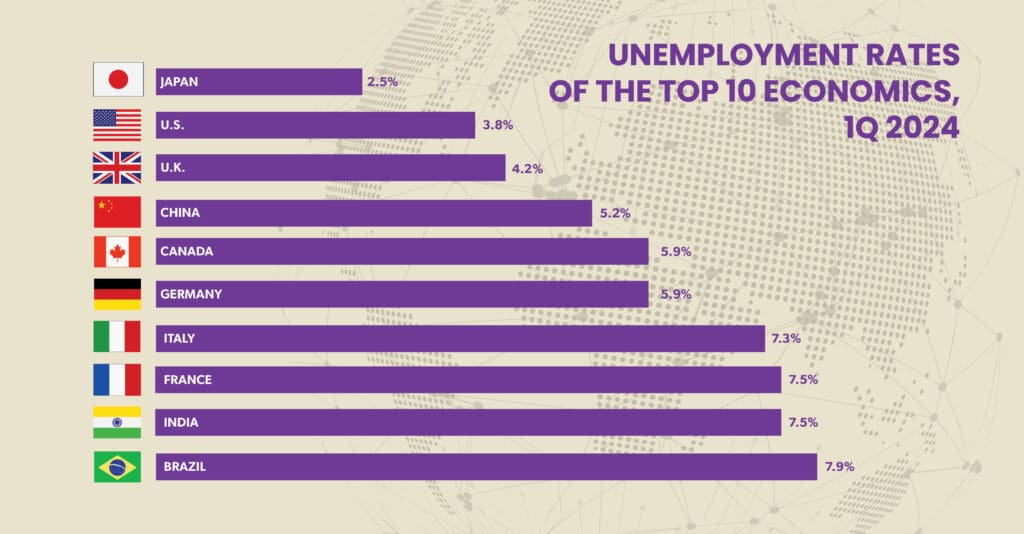

DRIVING THE ECONOMIC GROWTH ENGINE

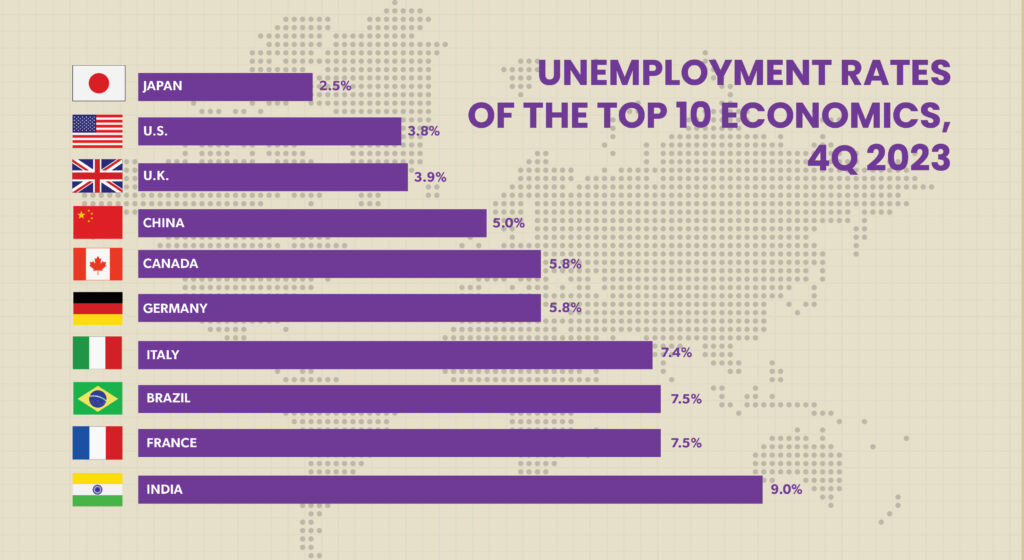

To explore international labor markets, companies must first consult global labor market data. PeopleScout, a global provider of RPO, MSP, and total workforce solutions, has partnered with HRO Today magazine to produce quarterly reports that compile current international labor market figures, including measures like national gross domestic product (GDP) and unemployment rates over time, from countries across the globe. This data reveals critical information about the state of the talent pool, working conditions, and recruitment needs of various countries and regions. It is an essential tool for predicting fruitful locations for expansion and recruitment, thereby allowing multinational companies to stay competitive in talent acquisition.

To explore international labor markets, companies must first consult global labor market data. PeopleScout, a global provider of RPO, MSP, and total workforce solutions, has partnered with HRO Today magazine to produce quarterly reports that compile current international labor market figures, including measures like national gross domestic product (GDP) and unemployment rates over time, from countries across the globe. This data reveals critical information about the state of the talent pool, working conditions, and recruitment needs of various countries and regions. It is an essential tool for predicting fruitful locations for expansion and recruitment, thereby allowing multinational companies to stay competitive in talent acquisition.

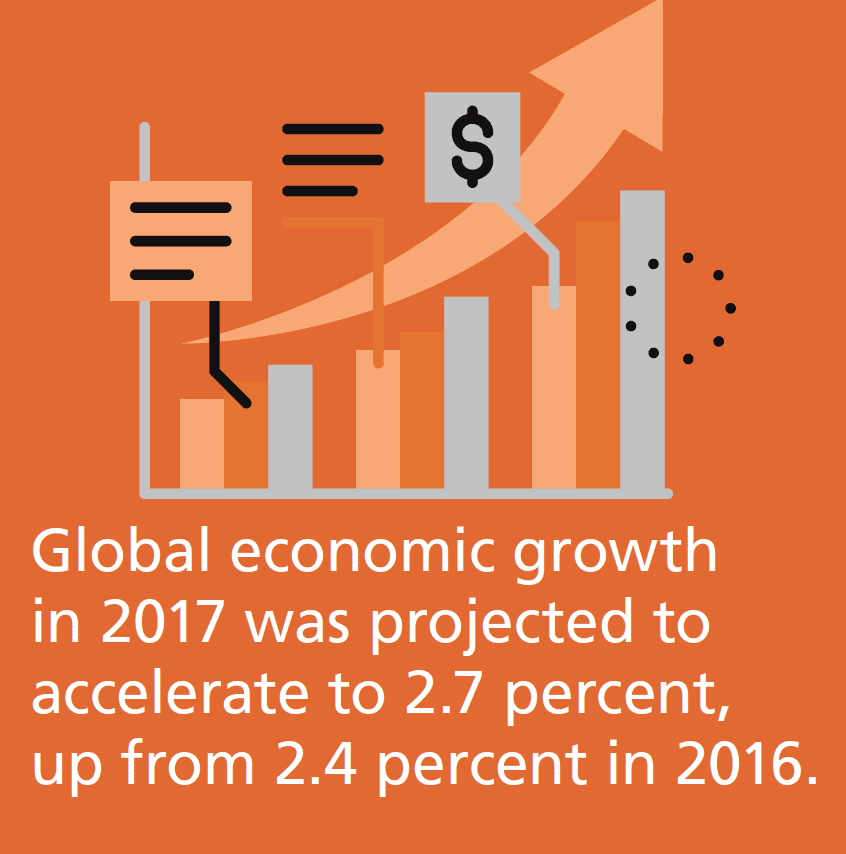

According to the World Bank’s June 2017 Global Economic Prospects report, global economic growth in 2017 was projected to accelerate to 2.7 percent, up from 2.4 percent in 2016. Activity in advanced economies driven by economic growth in the United States was expected to gain momentum in 2017, accelerating to 1.9 percent before moderating gradually in 2018 and 2019. In Europe and Japan, strengthening domestic demand and exports led to improved 2017 growth forecasts. Growth in emerging markets and developing economies was projected to reach 4.1 percent in 2017 and 4.5 percent in 2018.

According to the World Bank’s June 2017 Global Economic Prospects report, global economic growth in 2017 was projected to accelerate to 2.7 percent, up from 2.4 percent in 2016. Activity in advanced economies driven by economic growth in the United States was expected to gain momentum in 2017, accelerating to 1.9 percent before moderating gradually in 2018 and 2019. In Europe and Japan, strengthening domestic demand and exports led to improved 2017 growth forecasts. Growth in emerging markets and developing economies was projected to reach 4.1 percent in 2017 and 4.5 percent in 2018.

According to the Bureau of Economic Analysis, third quarter 2017 GDP grew at 3 percent in the United States, similar to the second quarter. The increase in real GDP results from increases in consumer spending, inventory investment, business investment, and exports on both goods and services. A notable offset to these increases was a decrease in housing investment. Imports, which are a subtraction from GDP, decreased, reports the Bureau of Economic Analysis.

In September, the U.S. unemployment rate declined slightly to 4.2 percent from 4.4 percent in June. The unemployment rate has remained below 5.0 percent since January 2016, suggesting stability in the American job market and conditions considered by many economists to be “fully employed.”

Unemployment in the EMEA region fell for nine of the 10 largest economies, with only Saudi Arabia reporting an uptick. The German economy is the largest in the EMEA region with a GDP of Intl $3,980 billion. Unemployment in Germany declined 0.3 percent to 3.6 percent in the third quarter of 2017.

See more here.

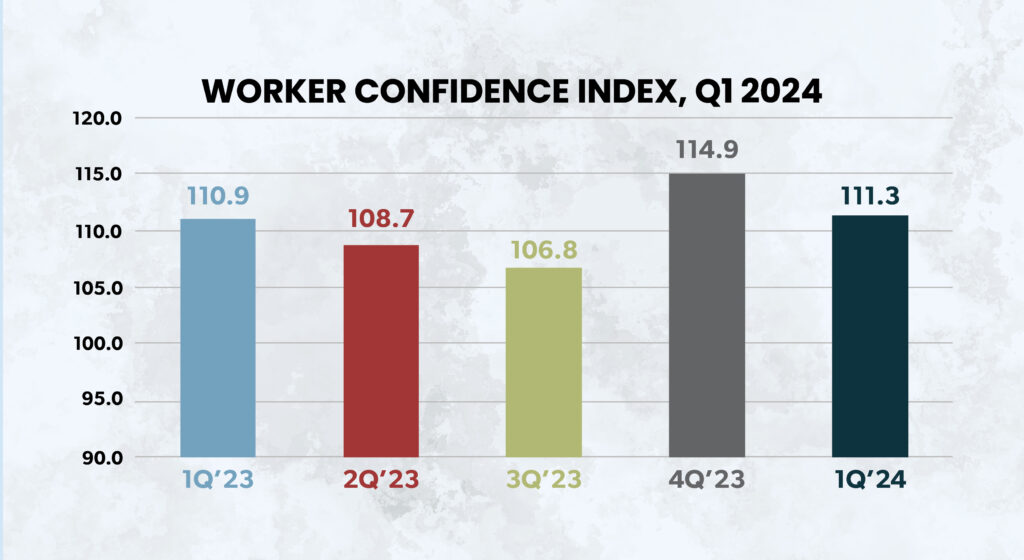

SHARING THE WEALTH?

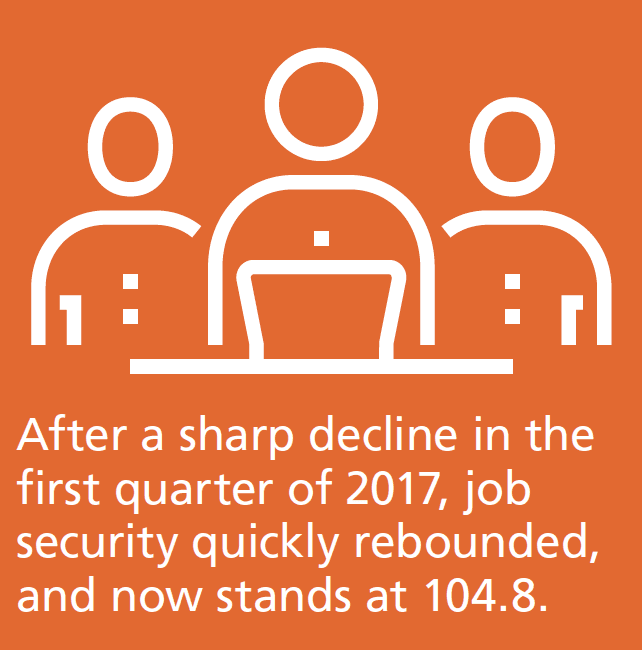

The Worker Confidence Index (WCI) for the third quarter of 2017 increased by 2.8 points after a significant drop of 7.9 points in the second quarter. WCI now stands at 102.5. Of the four components of the WCI, only likelihood of promotion rose by 3.2 points in the third quarter of 2017, while other components remained virtually the same. Other indicies -job stability, likelihood of raise, and trust in company leadership -measure similarly to the third quarter of 2016.

The Worker Confidence Index (WCI) for the third quarter of 2017 increased by 2.8 points after a significant drop of 7.9 points in the second quarter. WCI now stands at 102.5. Of the four components of the WCI, only likelihood of promotion rose by 3.2 points in the third quarter of 2017, while other components remained virtually the same. Other indicies -job stability, likelihood of raise, and trust in company leadership -measure similarly to the third quarter of 2016.

Workers remain secure about job stability. After a sharp decline in the first quarter of 2017, job security quickly rebounded, and now stands at 104.8, about where it was five quarters ago. Lack of concern about job loss is the most important indicator in estimating worker confidence about current and near-term financial outlook.

Females once again reported higher levels of confidence in job security than males in the third quarter of 2017. In fact, women reported the highest level of job security since the inception of the study. The percentage of males who felt that they would lose their job increased slightly to 11.4 percent from 10.5 percent in the prior quarter. Female concern over job security declined, down 2.1 percentage points from last quarter to 5.9 percent. Respondents over the age of 45 also reported feeling more secure about their job stability. Higher income employees (the $100,000-plus segment) reported having the most job security.

Females once again reported higher levels of confidence in job security than males in the third quarter of 2017. In fact, women reported the highest level of job security since the inception of the study. The percentage of males who felt that they would lose their job increased slightly to 11.4 percent from 10.5 percent in the prior quarter. Female concern over job security declined, down 2.1 percentage points from last quarter to 5.9 percent. Respondents over the age of 45 also reported feeling more secure about their job stability. Higher income employees (the $100,000-plus segment) reported having the most job security.

In 2017, trust in company leadership continued to decline steadily for the third consecutive quarter. Corresponding with that decline is a decrease in the belief in the likelihood of a raise of at least 3 percent. Workers tend to not trust management when they learn of positive earnings and then that success doesn’t translate to greater compensation for them. They may feel secure because the company is doing well, but trust isn’t necessarily established if the company’s positive result doesn’t result in increased compensation for employees. While two-thirds (63.8 percent) of the youngest respondents expressed confidence in their company’s leadership in the third quarter of 2017, trust in leadership declined steadily as age of respondents increased.

See more here.

IN JEOPARDY

Organizations have a strong need for top-tier background screening providers, and that need is increasing monthly. The pre-employment screening industry alone represents a $2 billion domestic market (according to research by IBISWorld), and that amount is expected to grow as more jobs are added that will need background checking. The U.S. Bureau of Labor Statistics’ 2017 forecast is 2.2 million jobs.

Organizations have a strong need for top-tier background screening providers, and that need is increasing monthly. The pre-employment screening industry alone represents a $2 billion domestic market (according to research by IBISWorld), and that amount is expected to grow as more jobs are added that will need background checking. The U.S. Bureau of Labor Statistics’ 2017 forecast is 2.2 million jobs.

Coupled with the needs to accommodate volume of hiring, HR in the U.S. faces hundreds of work-related homicides, billions of dollars in employee theft, and numerous applications with embellishments or outright lies annually. In fact, bad hires cost a company nearly $17,000 on average, which doesn’t include damage to employee morale, additional supervision time to train or turn around a bad hire, productivity loss for the organization, revenue that’s not being generated, and client relationships that could turn sour as a result of bad impressions.

To better determine the factors that HR practitioners use in assessing background screening services and the array of services that are most important to them, CSS Inc. (Comprehensive Screening Solutions) commissioned HRO Today to conduct a study among those directly involved with selecting background providers for their organizations across the U.S. The findings were clear: When it comes to the need for background screening, the stakes are higher now for companies than ever before. In a tight labor market, there’s enormous pressure to hire more employees quickly; in particular, data and physical security are paramount.

There is a lack of quantification about the impact of background screening providers. More than 77 percent of study respondents didn’t have or weren’t aware of any formal metrics for measuring the success of their background screening provider service. Although 86 percent of respondents are satisfied with their background screening providers, there was no hard evidence on which to base the opinion.

Often, HR departments don’t take background screening and the selection of screening providers seriously enough. It’s ironic that the primary way background screening providers are verified by HR practitioners is through references offered by the provider. That’s the equivalent of relying only on what a candidate tells a potential employer about their background.

The top-tier criteria for determining which background screening service is the right fit for an organization are accuracy, compliance, and responsiveness. All other factors are secondary.

See more here.

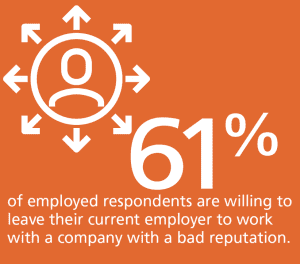

REPUTATION MATTERS

The impact of corporate reputation on employer brand is more significant than ever before and directly affects the cost of hiring, finds the 2017 The Cost of a Bad Reputation study from HRO Today and Cielo. This year’s results show that with the U.S. unemployment rate continuing to drop and the economy projected to expand moderately at 2.2 percent into 2018, organizations have to be more aware than ever of the impact of a bad reputation on their employer brand.

The impact of corporate reputation on employer brand is more significant than ever before and directly affects the cost of hiring, finds the 2017 The Cost of a Bad Reputation study from HRO Today and Cielo. This year’s results show that with the U.S. unemployment rate continuing to drop and the economy projected to expand moderately at 2.2 percent into 2018, organizations have to be more aware than ever of the impact of a bad reputation on their employer brand.

According to findings from this year’s study, 61 percent of currently employed respondents were willing to leave their current employer to work with a company with a bad reputation, about the same as the prior year. Males remain much more likely than females to take the job, at 69 percent versus 52 percent, respectively.

The percentage of females willing to take the job has declined for three straight years.

Among those candidates willing to join a company with a bad reputation, a pay increase of 58 percent is needed as enticement. On the other hand, candidates can be tempted to join a company with a good reputation with a significantly lower pay increase of 36 percent. Companies with bad reputations face increased recruiting costs due to the greater difficulty of sourcing and onboarding new hires. This is particularly true when recruiting females and more experienced workers.

And despite what is often reported, the youngest workers are the least concerned with company reputation, with 72 percent of millennials (aged 18 to 34) willing to take a job at a company with a damaged reputation compared to less than 60 percent of Gen X or baby boomers. Companies with such reputations may have fewer obstacles in recruiting this group if their other needs for, such as a positive work environment, flexibility, and advancement opportunities, are met.

A bad reputation affects more than just the cost of recruiting. If a company was involved in a major scandal, nearly three-quarters of its employees would look for a new job, most of them immediately. Additionally, over one-half (52 percent) of all those employed would start looking immediately, defined as less than 30 days. The result is a company-wide talent drain that would severely impact an organization’s ability to compete.

See more here.

FORGET FULL TIME

Recent research from HRO Today and Allegis Global Solutions found that the use of freelancers in the APAC region is growing rapidly, with 45 percent of respondents anticipating the use of freelancers will increase in the next 24 months. Use of freelancers over the prior two years also increased, albeit more modestly, as nearly a quarter of respondents reported an increase during that time.

Recent research from HRO Today and Allegis Global Solutions found that the use of freelancers in the APAC region is growing rapidly, with 45 percent of respondents anticipating the use of freelancers will increase in the next 24 months. Use of freelancers over the prior two years also increased, albeit more modestly, as nearly a quarter of respondents reported an increase during that time.

What positions do freelancers fill? Technology maintenance and development, such as website, IT, and software, were the most common job roles. In fact, freelance talent is also often applied more in the creative realm, graphic design, writing, and content.

Where do organizations source this talent? LinkedIn was the only source used by more than 50 percent of respondents; universities took the second spot, used by 48 percent of study participants. While LinkedIn seems to making inroads in APAC, only 35 percent of those respondents using it were satisfied, which suggests that progress in this region will be limited until the causes of dissatisfaction are determined and remedied.

The study also found that organizations leverage an array of sources for freelance talent, which is perhaps indicative of the broad scope of the APAC region. Only one source -LinkedIn -was used by over one-half of respondents (54 percent), suggesting that the social networking channel is making great headway in some of the APAC region, particularly in Hong Kong and Singapore. Other sources used with some degree of frequency include universities (48 percent) and internet job boards (44 percent).

See more here.

GAME ON?

A recent study from HRO Today and PeopleScout found that the use of gamification in human resources is still in its infancy in the APAC region and varies greatly in the individual countries that comprise this region. Where is it most popular? Talent acquisition and employee training programs see the value in adding gamification elements. It is also a great tool for building an organization’s talent pool.

A recent study from HRO Today and PeopleScout found that the use of gamification in human resources is still in its infancy in the APAC region and varies greatly in the individual countries that comprise this region. Where is it most popular? Talent acquisition and employee training programs see the value in adding gamification elements. It is also a great tool for building an organization’s talent pool.

Why are organizations considering gamification? The concept is an outgrowth of video games and companies looking for a competitive edge will want to interact with candidates in a way that’s familiar to them. Who will that be? The research found that Millennials, particularly males, are the demographic who will be first exposed to gamification.

For those organizations that have not implemented gamification, 26 percent plan to implement gamification within one year. On the other hand, 58 percent have no plans to leverage gamification strategies. Respondents indicating that they have either no plans to implement gamification or plans to implement gamification in over two years account for 66 percent of respondents, which suggest the total universe for gamification to be no more than one-third of companies in the APAC region.

Among the organizations that reported using gamification, 67 percent use it for both talent acquisition and training current employees. Gamification is being employed for more than just recruiting.

Keeping candidates engaged with the company is the most prevalent use of gamification, with 60 percent of respondents indicating they used it for that purpose. Forty percent of respondents leverage gamification for building the size of the talent pool. This is a strategy to keep candidates engaged.

See more here.

MISALIGNED AND MISSING OUT

Recent research from WilsonHCG and HRO Today found that all too often talent acquisition analytics and KPIs are not aligned with long-term goals and objectives. Nearly one-half (44 percent) of respondents are entirely focused on only short-term goals, with no focus on making strategic business decisions.

Recent research from WilsonHCG and HRO Today found that all too often talent acquisition analytics and KPIs are not aligned with long-term goals and objectives. Nearly one-half (44 percent) of respondents are entirely focused on only short-term goals, with no focus on making strategic business decisions.

Quality of hire was ranked as the most indicative measure when evaluating the success of the talent acquisition program. Retention is often a key component of the quality of hire metric, and is also frequently used as a metric to evaluate talent acquisition program success.

Less than two-thirds (63 percent) of survey respondents indicated that the talent acquisition model was integrated into the HR strategy, with only 22 percent indicating that it was completely integrated. A talent acquisition model that is only moderately integrated into the larger HR strategy cannot fully support the business strategy. One step toward aligning the objectives of the three areas is through a centralized talent acquisition budget, which only about one-half of HR respondents have.

See more here.

{kind=link}

{kind=link}