New research finds an increase in the desire and delivery of financial well-being benefits.

By Tom Kelly

In this pandemic economy, corporate budgets are being squeezed. But the need to provide both competitive benefit programs and cost-effective solutions is more important than ever. In response to COVID-19, many employers are looking to add benefits that can support emerging employee needs or fill gaps in current offerings.

Findings from Buck’s third annual Financial Wellbeing and Voluntary Benefits Survey makes it clear that employers understand workplace wellness programs need to go beyond physical health, encompassing emotional and social health as well. And in recent years, these programs have further expanded to include financial well-being -and not just retirement savings, but programs that tackle student loan debt, emergency savings, budgeting, and more. As employers look ahead and begin to plan for a return to business stability, holistic employee well-being will be a key concern. There are numerous research studies showing the link between reducing employee financial stress and improvements in engagement and productivity, including a recent report by The Consumer Financial Protection.

Of course, this year, employers face financial struggles too: sales slowdowns, supply chain interruptions, and in some cases, broken business models. Even though HR knows the importance of employee well-being, they also know they can’t afford to pile anything more onto the bottom line.

That’s why employers agree that new and evolving voluntary benefits -paid for by employees but at lower group rates -can help provide the flexibility and choice needed to overcome personal finance challenges. Voluntary benefits have now become the mainstream, with organizations on average offering more than 10 programs. Along with supplemental life insurance (80 percent), AD&D insurance (75 percent), and vision insurance (63 percent), the Financial Wellbeing and Voluntary Benefits Survey found the most commonly offered voluntary plans are:

- legal services (69 percent);

- critical illness (68 percent);

- health accident (64 percent);

- discounts (57 percent); and

- identity theft protection (55 percent).

At least 63 percent of respondents plan to expand their offerings in the near future. When asked why, one out of two employers cited financial well-being as the reason. Companies say they are most likely to add student loan guidance/refinancing (20 percent); student loan repayment (18 percent); hospital indemnity (13 percent); identity theft protection (12 percent); and long-term care (11 percent) to their list of offerings.

Participants also showed a growing interest in new products like college coaching, medical financing, addiction recovery, and DNA/genetic testing.

Improving the Bottom Line

As employers continue to further integrate and promote voluntary benefits, they are seeing increased economic returns.

Eighty percent say they see direct savings from voluntary benefits through attraction/retention (62 percent); behavior change (45 percent); increased participation in cost-favorable plans (30 percent); reduced premiums on employer-paid benefits (20 percent); and reduced health and welfare consulting (15 percent), administration (12 percent), or communications costs (10 percent).

The survey was conducted before the onset of the COVID-19 crisis. But even before the pandemic hit, employers were deeply aware of the financial stress many Americans struggle with every day. Survey respondents cited this as a top motivator for investing in financial well-being programs, backed up by research that shows that financial well-being is critical to promoting job satisfaction, loyalty, productivity, and engagement.

Now, as organizations navigate the impact of COVID-19 on the U.S. economy, financial well-being will become even more critical. Certain industries have been more affected than others and workers who have had wages reduced, been furloughed, or been re-hired after a period of unemployment may need extra support.

There is growing awareness that poor short-term financial decisions can have a lasting impact on employee financial health, including retirement readiness. The 2020 survey shows that 98 percent of employers want to offer their employees a unified and holistic financial well-being program. It’s also clear from responses that priorities have changed: budgeting, saving, credit card debt, and unexpected medical expenses top the list of program objectives. Only 38 percent of respondents listed “retire when ready” as their top financial well-being priority. Moving employees from financial instability to stability and, ultimately, to enhanced financial well-being requires removing short-term barriers such as student loan debt and paycheck-to-paycheck living.

There is growing awareness that poor short-term financial decisions can have a lasting impact on employee financial health, including retirement readiness. The 2020 survey shows that 98 percent of employers want to offer their employees a unified and holistic financial well-being program. It’s also clear from responses that priorities have changed: budgeting, saving, credit card debt, and unexpected medical expenses top the list of program objectives. Only 38 percent of respondents listed “retire when ready” as their top financial well-being priority. Moving employees from financial instability to stability and, ultimately, to enhanced financial well-being requires removing short-term barriers such as student loan debt and paycheck-to-paycheck living.

Half of survey participants agree that hourly employees are most in need of financial support. According to the U.S. Department of Labor, more than 78 million Americans are paid on an hourly basis. That’s 59 percent of the workforce and more than 71 percent of these workers are under age 30. Data shows that hourly workers struggle unnecessarily to move up and make more. By creating holistic financial well-being programs, employers expect to set their hourly employees up for continued financial success.

Forty percent of respondents said that millennials will also be top targets for financial support. Millennials are now the largest generation in the workforce. Many are saddled with student loans, consumer debt, and a lack of savings -both for emergencies and for retirement. Millennials need all the resources they can get to help them plan for the future, and companies believe that by offering them these resources, they will have the upper hand when it comes to recruiting young talent.

Voluntary Benefits Play a Key Role

Ninety-one percent of survey respondents agree that voluntary benefits help support financial well-being. In their newly evolved form, benefits can help address unexpected expenses, debt, and paycheck-to-paycheck issues:

- Fifteen percent of those surveyed said they would be interested in a “no credit check” financing option for unexpected expenses.

- Twelve percent of employers said they would be open to bill negotiation services.

- Ten percent would consider offering early, on-demand access to earned wages to help solve cash flow problems.

Through these benefits, employers hope to offer better alternatives to high-interest credit cards, 401(k) loans, overdraft fees, late fees, payday loans, or missed bill payments that compound financial stress. Organizations are also providing services like financial coaching programs, budgeting tools, bill pay services, guidance for establishing emergency funds, and professional credit counselling.

Supplemental Medical Playing a Bigger Role

The National Center for Health Statistics reported in February that one in seven people in the U.S. have problems paying their medical bills. That often means putting off treatment: There’s been a 30 percent decrease in cancer screenings and a 37 percent decrease in wellness visits as COVID-19 has forced delays in necessary healthcare. Ultimately, this will increase future claims by workers under company healthcare plans.

Supplemental medical plans can play a key role in “derisking” these higher healthcare costs, and continue to be viewed as highly effective in managing those costs. Hospital indemnity plans can offset out-of-pocket costs for increased hospitalizations. Plans like critical illness and health accident play a key role in helping employees prepare for unexpected medical expenses.

Seeing and Communicating Savings

The 2020 survey findings once again found that employers are changing the way they deliver and communicate voluntary benefits.

Fifty-eight percent of employers said integrating voluntary benefits with core enrollment was “extremely important” or “very important.” Fifty-three percent plan to integrate voluntary benefits with overall well-being strategy, while 54 percent plan to change the way they communicate voluntary benefits to increase visibility.

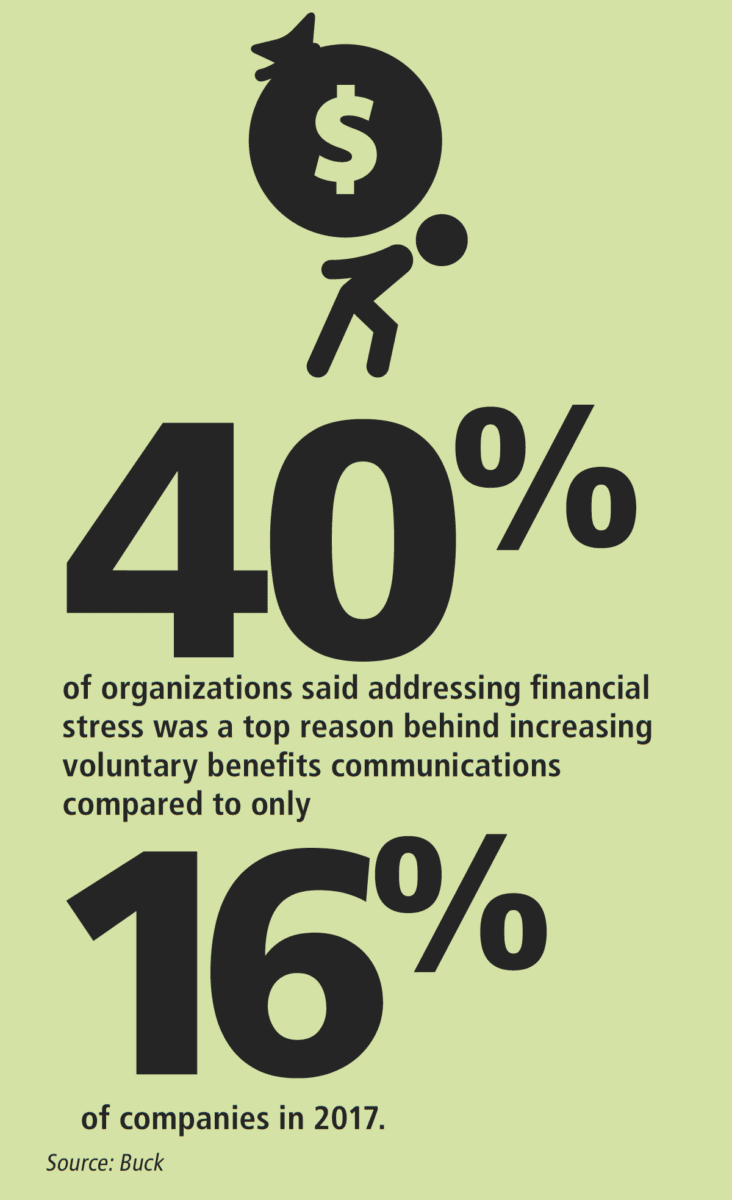

The survey found that 40 percent of employers said “addressing financial stress” was a top reason behind increasing voluntary benefits communications; this compares with only 16 percent of companies in 2017. In addition, 72 percent of employers view targeted communications as “extremely important” or “very important” to program success.

Instead of sharing generic product information, employers are using voluntary benefits communications to help employees gain the knowledge and confidence they need to use the benefits to improve their personal financial situation.

For the millions of employees living paycheck to paycheck, voluntary benefits options can help employees protect against unexpected expenses, provide access to needed cash, leverage financial coaching, or establish emergency funds. Through responsibly placed voluntary benefits, employers have an avenue to widen the scope of benefit offerings while also significantly decreasing the costs of delivering and administering benefit plans.

Tom Kelly is a principal in the health practice and the voluntary benefits practice leader of Buck.

{kind=link}

{kind=link}