Retirement comes faster than one may think. The time to plan is now.

By Ted Goldman

We all remember playing hide-and-seek as children and hearing the famous last words -ready or not, here I come -before the seeking begins. Whether you had found the perfect hiding place or not, the game was on. Well, whether you’ve prepared for retirement or not, it’s going to come. How you spend your retirement will depend on how well you prepared. The longer you wait, the harder it becomes. One thing is for certain: You can’t turn back the hands of the clock and start saving 10 years ago.

Emerging Issues

Over the last few years, there’s been a movement from defined benefit to defined contribution plans, resulting in the evolution of an emerging issue: retirement readiness. This is a term that probably as few as five years ago, didn’t even exist. Investopedia.com defines retirement readiness as follows:

The state and/or degree of being ready for retirement. Retirement readiness typically refers to being financially prepared for retirement, or the degree to which an individual is on target to meet his or her retirement- income goals so that the standard of living enjoyed while working will be maintained after retirement.

Notice that the definition is solely directed toward the individual who will be retiring. Nowhere does it indicate that one’s employer has a responsibility. Yet, employers can -and do -play an important role. The other phenomenon that is emerging is the term financial wellness. This seems to be a high priority for many organizations, but leaves HR professionals wondering what the organization’s role should be.

A recent report by the Consumer Financial Protection Board defines financial wellness as a state of being wherein the individual:

- Has control over day-to-day, month-to-month finances;

- Has capacity to absorb a financial shock;

- Is on track to meet financial goals; and

- Has the financial freedom to make the choices that allow the individual to enjoy life.

Clearly retirement readiness is under the umbrella of financial wellness. For some time now, employers have been providing wellness programs that incentivize healthy behaviors that relate to physical well-being. While the return on investment of these programs is hard to quantify, they are generally accepted as providing value. Expanding these programs to provide financial wellness is the next logical step.

Defining the Employer’s Role

There is an emerging debate as to what role organizations should play in supporting their employees with retirement readiness and financial wellness. It is now a standard agenda item at HR professional conferences and employers are taking these issues seriously. Organizations have several strategic decisions to make:

- Budget. Determine how much to budget for employee financial wellness and retirement readiness activities. Each organization has its own budget constraints. There is no right or wrong answer; it is a factor in attracting and retaining the right workforce for your organization.

- Approach. To get the most “bang for the buck,” consider which employees should benefit most from the financial investment, but also consider factors such as volatility and risk. The answers will determine if a defined contribution, defined benefit, or hybrid (such as a cash balance) retirement plan is the optimal retirement vehicle.

- Support. Determine how much support to provide in helping employees make good decisions regarding retirement and financial wellness. For example, the employer may choose to provide incentives to drive financially healthy behaviors or tools to help employees decide how much to save for retirement.

The cost or level of benefits is not the only indicator of the strength of a program. The effectiveness of a program should also be measured on whether it is achieving the desired outcomes that help the employer drive its business. An employer should be comparing the actual outcomes to those expected.

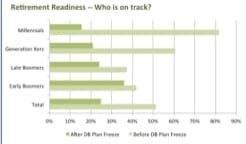

For example, one employer decided to freeze its traditional (defined benefit) pension plan and increase the 401(k) match from 50 percent to 100 percent match on the first 6 percent of employer contributions. Many employers now go “cold turkey” from a defined benefit to a defined contribution plan and do not take special efforts to offset potential benefit reductions for selected employee groups upon a plan change.

At first glance, the new 100 percent 401(k) match looked generous. However, the number of employees who were on a path to a secure retirement prior to the plan freeze and enhanced match was nearly 50 percent of the population, but after the plan change only 25 percent were on a path to a secure retirement.

Upon further study, it was determined that the Millennials were the hardest hit group. More than 80 percent of the Millennials were on a path to a secure retirement before the plan change, and post plan change, less than 20 percent were on target. Further analysis showed that all generational segments saw significant and uneven drops (see chart below). Using this outcomes-based approach to assessing plan effectiveness, this organization gained valuable insight as to where and how to refocus its support and available resources to help employees save for retirement.

Call to Action

The good news is that when there is a new problem on the horizon, it spurs innovative thinking and the quest to find solutions. Financial wellness and retirement readiness issues are clearly on this path. Today, there is no shortage of well-written educational material about how to plan for retirement. There are amazing tools and apps to help employees save and plan for a secure retirement. However, in spite of the availability of these great things, there has been minimal progress. Here are some real actions for employers to consider:

1. Identify the outcomes that will drive your business.

Work backwards from your business objectives to develop programs that will deliver the outcomes you need. For example, set a goal of having 80 percent of your workforce on a path to a secure retirement. Focus on the outcome.

2. Create the business case to take action. There is a direct benefit to the bottom line to help employees become more financially stable and be prepared for retirement:

• Financially unhealthy workforces create lost productivity through increases in absenteeism and lack of focus on work.

• Employers experience increased wage and benefit costs due to employees being unable to retire.

• An aging workforce creates talent management challenges, such as preventing or slowing advancement of high-potential staff.

• If the aging workforce is unable to retire, the result could be higher medical costs and severance costs (if layoffs are implemented).

You can calculate an expected return on investment if you successfully attain the outcomes you’ve established.

3. Adopt actions and solutions that have a high degree of impact. Like physical wellness efforts, you don’t want to end up with a basement full of barely used exercise equipment. Invest in outcomes-based programs that will make a difference. Examples of emerging solutions that can make a difference include next generation retirement programs that take automatic features to new levels, financial wellness incentive programs that drive good behaviors, and employee benefit portals that have the capability to drive personalized messages rather than a one-size-fits-all communication approach.

We clearly live in a defined-contribution world now. Employees are in the driver’s seat when it comes to responsibility for their own financial wellness and retirement readiness. However, most employees need some assistance. Organizations have a vantage point that allows them to play a key role in helping their employees achieve a greater level of financial wellness and be prepared for a secure retirement.

Ready or not, retirement is coming.

Ted Goldman is the retirement leader in the Wealth practice of Buck Consultants at Xerox.

{kind=link}

{kind=link}