An HRO recap of 2013 and 2014 outlook.

By Amy L. Gurchensky

2013 had a slow start, but a strong finish and proved to be a successful year for HR outsourcing services, with HRO contract activity up nearly 37 percent year-over-year. At the end of the first half of the year, the outlook did not look favorable. But bubbling second-half benefits administration activity—particularly health exchange contracts—allowed 2013 to finish well.

Some highlights for 2013:

Payroll. According to NelsonHall’s HRO Market Forecast: 2013 – 2017, the payroll market is one of the largest and most mature HRO service lines, and it will continue to grow with

a low single-digit compounded average annual growth rate (CAAGR) through 2017. Approximately 80 percent of the payroll contract activity in 2013 was from the mid-market (organizations with between 500 and 15,000 employees). These deals typically involved a single country.

In addition to contract activity, there was a great focus on payroll expanding its global reach, particularly within Latin America and Asia Pacific.

• ADP acquired Payroll S.A., and expanded its Latin America payroll capabilities to Chile, Argentina, and Peru.

• CloudPay opened an office in Sao Paulo to expand its payroll capability in Brazil by partnering with Apdata.

• Safeguard World International opened a larger office in Mexico to support its growth; and

• Acrede launched an office in Singapore.

Recruitment process outsourcing (RPO). According to NelsonHall estimates, RPO is the fastest growing HRO service line with a mid-teen double-digit CAAGR through 2017.

One of the biggest announcements in RPO in 2013 was the merger of Pinstripe and Ochre House to deliver global RPO. Multi-country RPO activity started gaining some traction in the market in the second half of 2010. Contract examples include Manpower and Rio Tinto (Australia, Canada, France, South Africa, U.S., South America, U.K., India, and the Middle East) and FutureStep and Cummins Inc. (across 50 countries in North America, Europe, Asia Pacific, and South America).

Fast-forward to 2013, and multi-country activity accounted for nearly 25 percent of all RPO contracts. Manpower had two impressive contracts in terms of scope: One deal covered 37 countries across multiple continents, and the other covered 17 countries in Europe.

Although the Pinstripe and Ochre House merger wasn’t all too surprising since the two companies have been partnering since 2009, it is still big news as the combined companies now have RPO capabilities in 43 countries including the Middle East and North Africa, which Ochre House established through its acquisition of TAAHEED and Carmichael Fisher in 2012. Integration will take time, but once complete, the new entity will surely be a main contender for multi-country RPO.

Benefits administration. Benefits administration has been the main source of contract activity in the second half of 2013, particularly exchanges. By benefits administration service line, 2013 contract activity was distributed as follows:

• 52 percent health and wellness (H&W) services, including exchanges;

• 45 percent pension and retirement administration (DB and DC administration); and

• 3 percent flexible benefits administration.

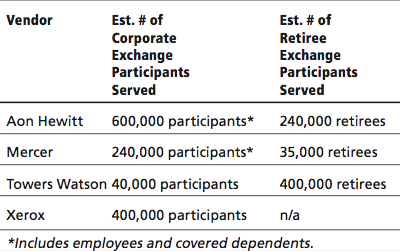

H&W contracts include a variety of H&W services including H&W administration, reimbursement account administration, leave of absence administration, health exchanges, etc. Approximately half of contract activity in 2013 was for exchanges. A synopsis of exchange contract activity by vendor is as follows:

Within the pension and retirement administration market, DC administration contracts continue to make strides globally. In 2013, DC admin contracts accounted for nearly 65 percent of contracts; the remaining 35 percent was DB admin contracts, most of which occurred in the U.K.

Outside of reimbursement account administration and exchanges, partnerships and merger and acquisition (M&S) activity within benefits administration was fairly distributed among the other service lines.

WageWorks started 2013 by acquiring Benefit Concepts to strengthen its reimbursement account and COBRA administration capabilities. Later in the year, Towers Watson and Ceridian both established partnerships with WageWorks:

• Towers Watson for health account administration including HRAs and HSAs for its private health insurance exchange; and

• Ceridian transitioning its existing nearly 18,000 reimbursement account admin clients to WageWorks who will then provide administration for FSAs, HRAs, HSAs, commuter benefits accounts; Ceridian is also transitioning its cafeteria plan/premium only plan business to WageWorks.

• Even though health exchanges are a fairly new offering in the market, partnership and M&A activity began

in this area as well in 2013. On the partnership front, activity was focused on retiree exchanges:

• Fidelity partnered with Extend Health, a Towers Watson company to provide retiree healthcare services.

• Aon Hewitt partnered with National Council on Aging to provide seniors with access to find affordable healthcare and prescription drug coverage through Aon Hewitt Navigators.

On the private exchange side, Guardian partnered with Liazon in July to offer a private benefits exchange, and in November, Towers Watson announced its acquisition of Liazon for $215m to enhance its exchange offering, adding Liazon’s private benefits exchange for active employees to its exchange portfolio.

Multi-process HRO (MPHRO). The MPHRO market has been relatively quiet the last few years and 2013 was no exception. While there hasn’t been significant news, the market is still growing slowly, but surely. New MPHRO contracts are still being awarded, and in 2013 they came from many different regions including the Nordics and the Middle East.

Single-country MPHRO contracts outpaced multi-country ones as did mid-market deals versus large market ones. The use of Workday is also increasing in MPHRO deals, namely by Aon Hewitt after its acquisition of OmniPoint Workday Solutions in late 2012.

Learning. The learning market has arguably been the slowest HRO service line to recover from the recession. Nevertheless, organizations are investing in learning again, and 2013 had the highest growth rate since 2007, driven by the need for job skill training and talent development.

In the past few years, the majority of learning contract activity has been from the public sector, but private sector activity picked up in 2013, and in multiple geographies. For example:

• Raytheon was awarded a multi-million dollar learning BPO contract by General Motors in Korea.

• Xerox was awarded a five-year learning BPO contract by OMV in Austria.

• GP Strategies was awarded a multi-year global learning BPO contract by HSBC.

• Infosys was awarded a two-year learning BPO contract by a multi-national pharma and biologics company in the U.K.

NelsonHall’s latest Targeting Learning BPO market analysis report also found that while selective-learning BPO contracts outnumber full-learning BPO contracts, there has been a resurgence for full-learning BPO contract since mid-2012, as evidenced by the above examples as well.

2013 also had several acquisitions in the learning space with nearly 80 percent focused on strengthening learning offerings including:

• Capita acquired KnowledgePool to enhance its managed learning services.

• Xerox acquired LearnSomething to strengthen its custom e-learning services and consumer education to the food, drug, and healthcare industries.

• GP Strategies in particular had a very busy year with partnerships and M&A’s for its learning offering. The company:

– Acquired Lorien Engineering Solutions to expand its learning services capabilities in the U.K. and Poland;

– Acquired Prospero Learning Solutions to strengthen its learning content development capability in Canada; and

-Partnered with Information Technology Senior Management Forum to launch an innovation and creativity learning portal.

Spotlight on 2104

2014 has the potential for more growth. Here are some predictions for what to expect this year:

Payroll. Due to changing tax laws and regulations, both domestically and internationally, growth for payroll services will be driven by compliance and the need to reduce risk. As with 2013, the mid-market is expected to account for the majority of contract activity in 2014, especially as demand for platform-based payroll services remains high. Within

the large market, multi-country payroll will see double- digit growth as multinational organizations continue to standardize and consolidate onto one global platform. Latin America and Asia Pacific will experience the most traction as suppliers gain momentum on plans they initiated in 2013.

RPO. As demand for multi-country RPO continues, we can expect to see more M&A and partnership activity in RPO. Talent shortages remain a widespread problem and lead

to increases for services such as employer branding and talent pool development. In addition, onboarding will become more robust as will the focus on processes such as employee engagement and retention strategies. In an effort to develop optimal workforce strategies—blending RPO and managed services programs for temporary hiring—will increase.

Benefits administration. H&W services will continue to dominate the benefits administration landscape, driven by compliance and the need to control the rising cost of healthcare through DC benefit plans. In particular, exchange contracts for active employees and retirees, as well as H&W services will further penetrate the market. There will also be more exchange partnership activity.

In the U.S., demand for DB and DC core services will primarily consist of second-generation contracts. Service providers will continue to develop offerings including:

• Adding standard enrollment wizards that allow DC plan sponsors to set defaults and participants to enroll quickly;

• Expanding non-qualified offerings; and

• Ensuring compliance with fiduciary and fee disclosure rules.

MPHRO. In 2014, the MPHRO offering will continue to be structured around a core model of services including HR administration, payroll, and contact center. Recruitment services will be the most popular add-on for the next 12 to 24 months as organizations focus on adding back talent. In the near-medium term, demand will increase for learning, performance, and compensation administration. The proportion of mid-market clients will grow, making up the greater share of new contracts and MPHRO pipelines, especially as cloud-based offerings become more prevalent.

Learning. Due to the emphasis on attracting, developing, and retaining talent, organizations will increase learning budgets for job skill training and professional development. Selective-learning BPO contracts will outpace full-learning BPO, led by content development including the conversion of ILT to e-learning. However, full-learning BPO contracts will appear more as clients re-invest in learning and do not want to rebuild their internal learning organizations. Supplier focus will be on strengthening and integrating talent management services and technology offerings.

Based on these expectations, 2014 will be another exciting year in HR outsourcing.

Amy L. Gurchensky is principal HRO analyst for NelsonHall.